Many foreign investors believe capital gains tax in Portugal is either non-existent or straightforward, leading to costly surprises at sale time. The reality is more nuanced. Portugal does levy capital gains tax on property sales by non-residents, with specific rates, exemptions, and filing requirements that directly impact your investment returns. Understanding these 2026 rules is essential for making informed decisions about buying, holding, and selling Algarve real estate. This guide breaks down the taxation framework, calculation methods, available exemptions, and practical compliance steps tailored specifically for foreign property investors in Portugal.

Table of Contents

- Understanding Capital Gains Tax In Portugal: Basics For Foreign Investors

- How Capital Gains Tax Is Calculated On Portuguese Property Sales

- Exemptions, Deductions, And Special Rules Impacting Capital Gains Tax

- Practical Steps And Filing Requirements For Foreign Investors In Portugal

- Learn More About Investing In Algarve Real Estate With Riva Prime

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Tax applies to all | Capital gains tax in Portugal applies to both residents and non-residents on property sales, impacting foreign investors directly. |

| Calculation is specific | Tax is computed on profit using acquisition cost, sale price, and allowable deductions with rates up to 28% for non-residents. |

| Exemptions exist | Reinvestment relief and primary residence exemptions can significantly reduce or eliminate tax liability for qualifying investors. |

| Filing is mandatory | Non-residents must submit Portuguese tax returns within specific deadlines or face penalties and legal complications. |

| Professional help matters | Complex rules and documentation requirements make expert tax and legal guidance valuable for compliance and optimization. |

Understanding capital gains tax in Portugal: basics for foreign investors

Capital gains tax in Portugal is a levy on the profit you realize when selling property. For foreign investors, this tax applies regardless of residency status. Capital gains tax in Portugal applies to both residents and non-residents on property sales, meaning your Algarve investment property is subject to taxation when you sell. The Portuguese tax authority, Autoridade Tributária e Aduaneira, treats capital gains as income, taxing the difference between your purchase price and sale price after allowable deductions.

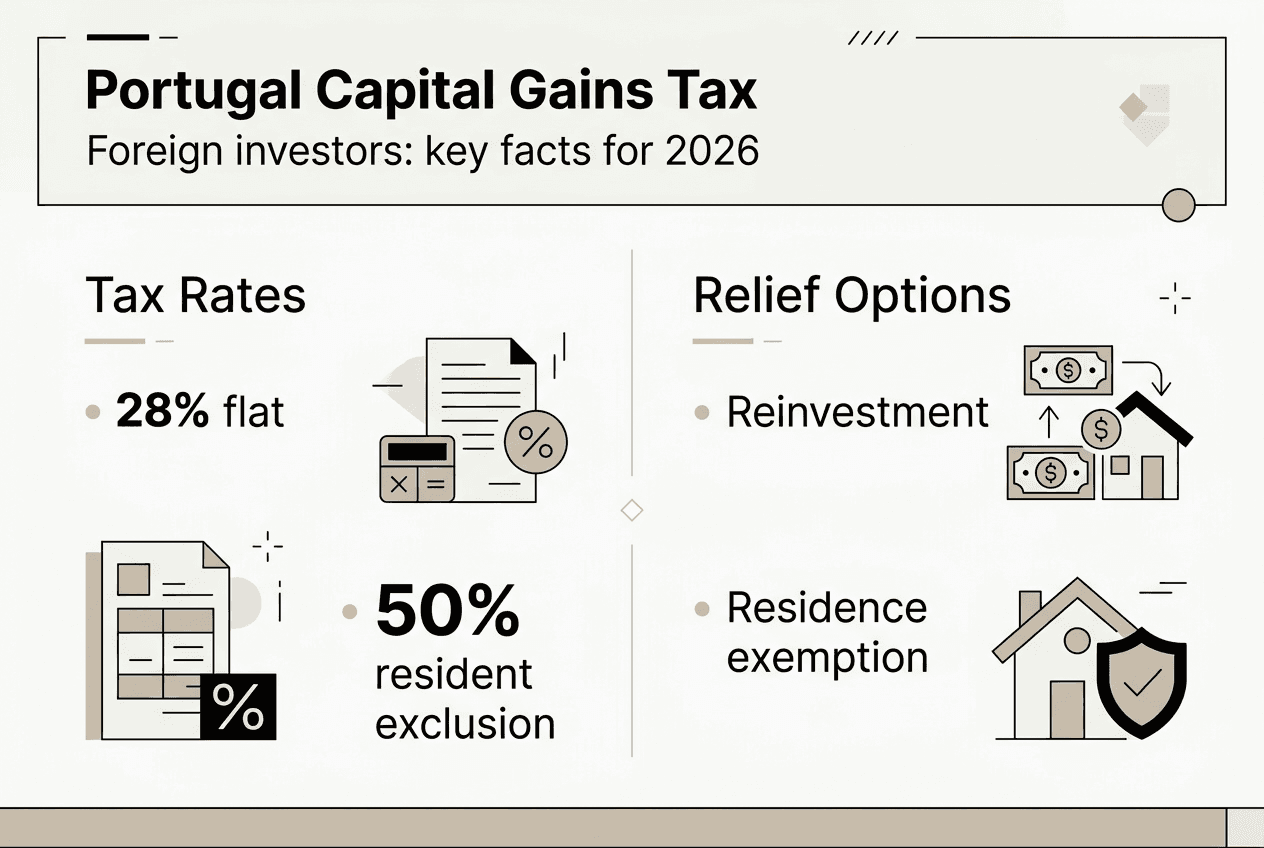

Non-resident individuals face a flat rate of 28% on their capital gains from Portuguese property sales in 2026. This contrasts with residents who benefit from progressive income tax rates and can include only 50% of their gains in taxable income, effectively reducing their burden. Companies and corporate entities face different rates, typically 25% on gains. These distinctions matter significantly when structuring your investment.

Foreign sellers must register with Portuguese tax authorities and obtain a fiscal number before completing any property transaction. You are required to file a tax return declaring your capital gains even if you owe no tax due to exemptions. This filing obligation exists separately from the transaction itself. Many investors mistakenly assume their home country’s tax treaty eliminates Portuguese obligations, but treaties typically allow Portugal to tax property gains within its borders while providing foreign tax credits to avoid double taxation.

Understanding foreign ownership rules Portugal 2026 helps contextualize these tax requirements within the broader legal framework. The key takeaway is that selling Portuguese property triggers a taxable event requiring compliance with local tax law, regardless of where you live or hold citizenship.

Pro Tip: Obtain your Portuguese fiscal number and register with tax authorities immediately after purchasing property, not when you plan to sell. This simplifies future compliance and ensures you receive official correspondence about tax obligations.

- Non-residents pay a flat 28% rate on capital gains from property sales

- Residents can exclude 50% of gains and use progressive rates

- Corporate entities typically face a 25% rate on property gains

- Tax registration and filing are mandatory regardless of exemption eligibility

- Double taxation treaties provide credits, not exemptions from Portuguese tax

How capital gains tax is calculated on Portuguese property sales

Capital gains tax is calculated based on the difference between sale price and acquisition cost, adjusted for allowable expenses. The formula starts simple but incorporates several adjustments that can substantially reduce your taxable gain. Understanding each component helps you plan deductions and estimate your tax liability accurately before listing your property.

The basic calculation follows this structure:

- Determine your acquisition cost, including purchase price, notary fees, registration costs, and real estate agent commissions paid when buying

- Add documented improvement costs like renovations, extensions, or major upgrades that increased property value

- Calculate your net sale price by subtracting selling costs such as agent commissions, legal fees, and marketing expenses

- Subtract the adjusted acquisition cost from net sale price to arrive at your taxable capital gain

- Apply the 28% non-resident rate to this gain to determine tax owed

Currency fluctuations between purchase and sale can work in your favor or against you. Portuguese tax authorities calculate gains in euros, so if you purchased when the euro was stronger against your home currency, your euro-denominated gain may be lower than your perceived profit. Keep detailed records of exchange rates at transaction dates.

Consider this example: You purchased an Algarve villa for €300,000 in 2020, paying €15,000 in acquisition costs. You invested €50,000 in renovations with proper invoices. In 2026, you sell for €450,000, paying €22,500 in agent commissions and €3,000 in legal fees. Your calculation would be:

| Component | Amount (€) |

|---|---|

| Sale price | 450,000 |

| Minus selling costs | (25,500) |

| Net sale proceeds | 424,500 |

| Original purchase price | (300,000) |

| Acquisition costs | (15,000) |

| Documented improvements | (50,000) |

| Taxable capital gain | 59,500 |

| Tax at 28% | 16,660 |

This example shows how proper documentation of improvements and costs reduces your taxable gain from €150,000 to €59,500, saving you over €25,000 in taxes. Understanding rental income taxation Portugal 2026 also helps if you generated rental income during ownership, as some expenses may be relevant to both income and capital gains calculations.

Pro Tip: Keep every invoice, receipt, and bank transfer record related to property improvements in a dedicated file. Portuguese tax authorities require original documentation, and missing paperwork means lost deductions worth thousands in additional tax.

Exemptions, deductions, and special rules impacting capital gains tax

Portugal offers specific exemptions and deductions such as reinvestment relief and primary residence exemptions. These provisions can dramatically reduce or eliminate your tax liability if you meet specific conditions. Foreign investors often overlook these opportunities, paying more tax than legally required.

The reinvestment exemption allows you to defer capital gains tax if you reinvest sale proceeds into another Portuguese property within specific timeframes. For residents, this exemption applies when purchasing a primary residence within 36 months before or 24 months after the sale. Non-residents face more restrictive conditions but can still benefit if they establish residency or invest in qualifying Portuguese real estate. The exemption amount is proportional to the reinvested percentage, so reinvesting 70% of proceeds exempts 70% of your gain.

Primary residence exemptions offer the most significant tax relief but primarily benefit residents. If you lived in the property as your main home for at least 12 months and are over 65, or if you reinvest in another Portuguese primary residence, you may exclude gains entirely. Non-residents rarely qualify unless they become tax residents before selling. This creates a strategic consideration: establishing Portuguese residency before sale could save substantial tax if you meet the time requirements.

Residents enjoy an additional advantage beyond exemptions. They can exclude 50% of their capital gains from taxable income automatically, then apply progressive income tax rates to the remaining 50%. This effectively halves the tax rate compared to the flat 28% non-resident rate. A resident in a 35% tax bracket pays just 17.5% effective rate on gains, while non-residents pay the full 28%.

| Taxpayer Type | Gain Inclusion | Tax Rate | Effective Rate |

| — | — | — |

| Non-resident | 100% | 28% flat | 28% |

| Resident | 50% | Progressive (14.5%-48%) | 7.25%-24% |

| Resident with reinvestment | 0%-100% | Progressive | 0%-24% |

Tax treaties between Portugal and your home country may provide additional relief through foreign tax credits. Most treaties allow Portugal to tax property gains but require your home country to credit the Portuguese tax against your domestic liability. This prevents double taxation but does not reduce the Portuguese tax itself. Review your specific treaty provisions with a qualified advisor.

Understanding these rules connects directly to broader property investment tips Portugal that help you structure ownership and timing for optimal tax treatment. The differences between resident and non-resident treatment are substantial enough to influence holding period and residency decisions.

- Reinvestment exemption defers tax when proceeds fund another Portuguese property purchase

- Primary residence exemption eliminates tax for qualifying residents meeting occupancy requirements

- Residents automatically exclude 50% of gains and benefit from progressive rates

- Non-residents face flat 28% on full gain with limited exemption access

- Tax treaties provide foreign tax credits but do not reduce Portuguese tax owed

Practical steps and filing requirements for foreign investors in Portugal

Compliance with Portuguese capital gains tax requirements involves specific documentation, deadlines, and procedures that foreign investors must follow precisely. Non-resident property owners must file Portuguese tax returns reporting capital gains within specified deadlines to avoid penalties. Understanding this process helps you avoid costly mistakes and legal complications.

The filing process follows these steps:

- Obtain or verify your Portuguese fiscal number (NIF) is active and your tax registration is current

- Gather complete documentation including purchase deed, sale deed, improvement invoices, and expense receipts

- Calculate your capital gain using the methodology outlined earlier, with all amounts in euros

- Complete Form 3 (Modelo 3), the Portuguese individual income tax return, declaring your capital gain

- Submit your return electronically through the Portuguese tax authority portal or via a fiscal representative

- Pay any tax owed by the deadline to avoid interest and penalties

Non-residents must file their return by May 31st of the year following the sale. If you sold property in 2026, your return is due by May 31, 2027. However, Portuguese tax law requires withholding at source for non-resident sellers. The buyer’s lawyer typically withholds 28% of the gain at closing and remits it to tax authorities. You then file your return to claim any overpayment refund if deductions or exemptions reduce your actual liability below the withheld amount.

Documentation requirements are strict. You need original invoices for all claimed deductions, bank statements proving payments, and certified translations of foreign documents if authorities request them. The purchase and sale deeds must clearly show transaction values, and any improvements require contractor invoices with proper VAT documentation. Missing or inadequate documentation means authorities will disallow deductions, increasing your tax.

Penalties for non-compliance escalate quickly. Late filing incurs fines starting at €200 and increasing based on delay duration. Late payment adds interest at statutory rates plus penalties of 10% to 50% of unpaid tax depending on whether authorities consider the failure negligent or intentional. In severe cases, authorities can place liens on Portuguese assets or pursue collection through international agreements.

Given the complexity and language barriers, most foreign investors benefit from professional assistance. Portuguese tax advisors and lawyers specializing in real estate transactions can prepare returns, communicate with authorities, and optimize your tax position within legal boundaries. The cost of professional help, typically €500 to €2,000 depending on complexity, often saves multiples of that amount through proper deduction documentation and exemption application. Explore legal assistance for property buyers to connect with qualified professionals.

- File Form 3 by May 31st following the year of sale

- Expect 28% withholding at closing, then file to claim refunds

- Keep original invoices, deeds, and payment records for all deductions

- Late filing penalties start at €200 and increase with delay

- Professional tax assistance typically costs €500-€2,000 but often saves much more

Pro Tip: Appoint a fiscal representative in Portugal if you do not maintain a Portuguese address. This representative receives official tax correspondence and ensures you do not miss critical deadlines due to mail delays or language issues.

Learn more about investing in Algarve real estate with Riva Prime

Navigating capital gains tax is just one aspect of successful property investment in Portugal. Riva Prime specializes in helping foreign investors understand and profit from Algarve real estate opportunities while managing all the complex legal, tax, and operational details. Our team guides you through every stage, from identifying high-potential properties to optimizing your tax position and managing rental income.

Whether you are exploring your first Portuguese property purchase or planning an exit strategy for existing holdings, understanding the complete investment lifecycle helps you maximize returns. Our comprehensive resources cover everything from steps to invest in Algarve real estate to ongoing property investment tips Portugal that address tax planning, market timing, and property management. We also connect you with trusted legal assistance for property buyers who can handle your tax filings and ensure full compliance with Portuguese law. Contact Riva Prime to discuss how we can support your Algarve investment goals.

Frequently asked questions

What is the capital gains tax rate for non-residents on property sales in Portugal?

Non-residents pay a flat 28% rate on capital gains from Portuguese property sales in 2026. This rate applies to the full gain after deducting acquisition costs, improvements, and selling expenses. Residents benefit from lower effective rates by excluding 50% of gains and using progressive income tax brackets.

Are there any exemptions for reinvesting proceeds into other Portuguese properties?

Yes, Portugal offers reinvestment relief that can defer or eliminate capital gains tax if you reinvest sale proceeds into another qualifying Portuguese property. Residents have broader access to this exemption, particularly for primary residence purchases within 36 months before or 24 months after the sale. Non-residents face more restrictive conditions but may qualify in specific circumstances.

How and when must foreign investors file their capital gains tax returns?

Foreign investors must file Form 3 (Modelo 3) by May 31st of the year following the property sale. For a 2026 sale, the deadline is May 31, 2027. Buyers typically withhold 28% of the gain at closing and remit it to tax authorities, with sellers filing returns afterward to claim refunds if their actual liability is lower due to deductions or exemptions.

Can tax treaties between Portugal and other countries reduce or eliminate capital gains tax?

Tax treaties generally allow Portugal to tax gains on Portuguese property while requiring your home country to provide foreign tax credits against your domestic tax liability. This prevents double taxation but does not reduce the Portuguese tax itself. Review your specific treaty with a qualified advisor to understand how credits apply to your situation.

What documents do foreign investors need to keep for capital gains tax purposes?

You must retain original purchase and sale deeds, all invoices for property improvements with proper VAT documentation, receipts for acquisition and selling costs, bank statements proving payments, and records of exchange rates at transaction dates. Portuguese tax authorities require original documentation to approve deductions, and missing paperwork results in disallowed deductions and higher tax bills.