Many foreign investors assume they can claim deductions against rental income tax in Portugal like they do back home. That’s wrong. Non-residents face a flat 28% tax with zero deductions allowed. Portugal’s 2026 tax reforms complicate the picture further, introducing a favorable 10% rate for specific long-term rentals while raising acquisition taxes. This guide cuts through the confusion, clarifying residency effects, new rules, and practical strategies to optimize your Algarve rental returns.

Table des matières

- Introduction To Rental Income Taxation In Portugal

- Portuguese Personal Income Tax System And Residency Implications

- 2026 Rental Income Tax Reforms And Their Impact

- Allowable Deductions To Optimize Rental Taxation

- Resident Vs Non-Resident Taxation On Rental Income

- Interaction With Non-Habitual Residency (NHR) Regime

- Common Misconceptions About Rental Income Tax In Portugal

- Practical Steps For Foreign Investors To Optimize Rental Income Tax

- Optimize Your Algarve Property Investment With Riva Prime

- FAQ

Key takeaways

| Point | Détails |

|---|---|

| Residency determines your tax rate | Residents pay progressive IRS rates of 12.5% to 48%, while non-residents face a flat 28% with no deductions. |

| 2026 reforms favor long-term rentals | A new 10% IRS rate applies to registered long-term leases capped at €2,300 monthly rent. |

| Non-residents cannot claim deductions | The 28% flat tax applies to gross rental income without expense offsets. |

| Acquisition taxes increased | Non-resident buyers now pay a 7.5% IMT property transaction tax, raising upfront investment costs. |

| Ownership structure matters | Individual landlords qualify for the 10% rate, while companies face corporate tax rules with partial reductions. |

Introduction to rental income taxation in Portugal

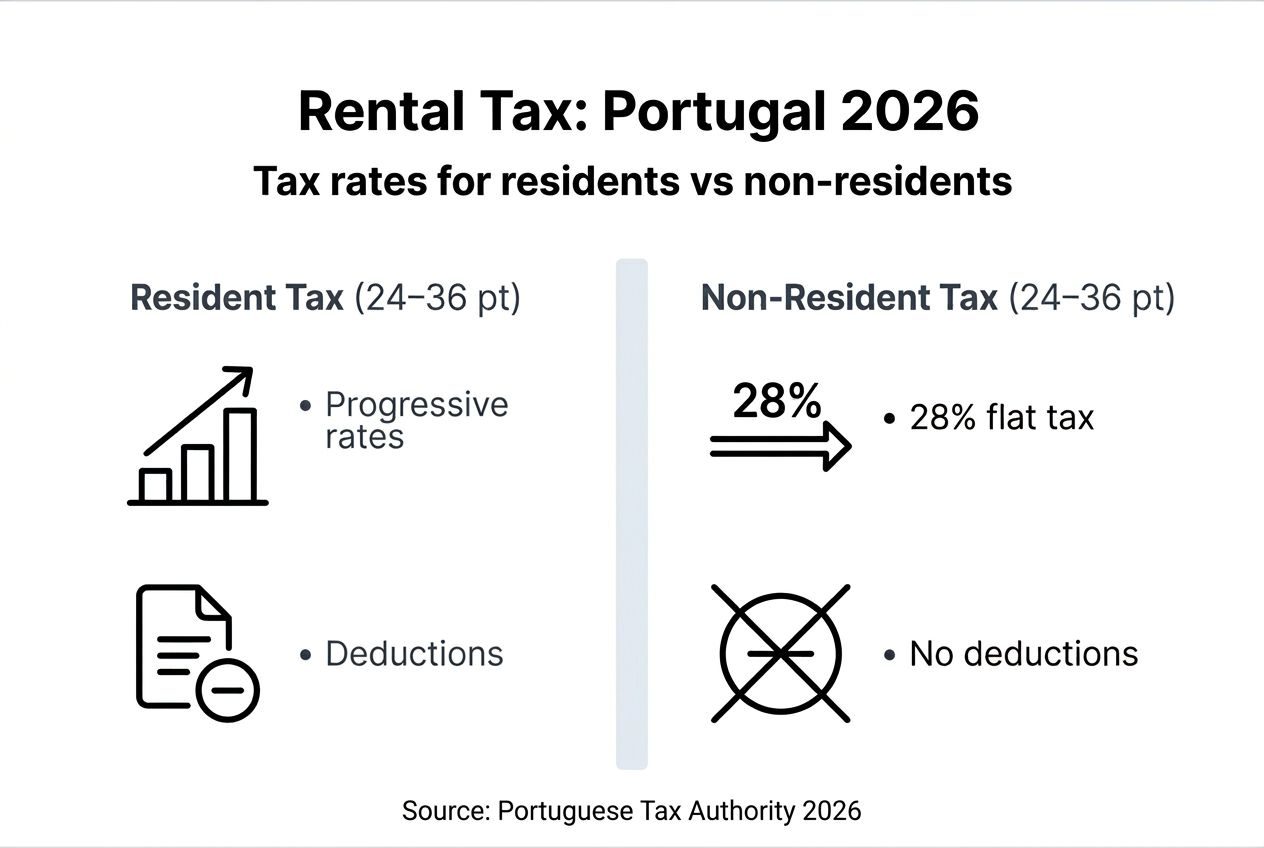

Portugal taxes rental income through its IRS (Personal Income Tax) system. Rental income falls under Category F, a distinct category from employment or business income. Your tax obligations depend entirely on whether you qualify as a tax resident or non-resident. Tax residents pay progressive IRS rates on worldwide income, ranging from 12.5% to 48% depending on total annual earnings. Non-residents pay a flat 28% tax on Portuguese-sourced rental income only.

Determining your residency status is critical. You become a Portuguese tax resident if you spend more than 183 days in Portugal during a calendar year, or if you maintain a permanent residence there by December 31. Getting this classification wrong leads to incorrect filings, penalties, and missed tax optimization opportunities. The distinction affects not just your tax rate but also your ability to claim deductions, your filing obligations, and your overall investment strategy.

Key differences between resident and non-resident taxation include:

- Income scope: Residents are taxed on worldwide income, non-residents only on Portuguese-sourced income

- Tax rates: Residents face progressive brackets, non-residents a flat 28%

- Deductions: Residents can deduct qualifying expenses, non-residents cannot

- Filing complexity: Residents submit comprehensive annual returns, non-residents have simpler obligations

- Strategic flexibility: Residency status affects eligibility for special tax regimes and optimization strategies

For foreign investors targeting short-term letting in Algarve markets, understanding these fundamentals prevents costly mistakes. The rental income tax guide published by Portuguese tax advisors confirms these distinctions between residents and non-residents remain foundational to compliance.

Portuguese personal income tax system and residency implications

Portuguese tax residents face progressive IRS brackets that climb steeply. The system starts at 12.5% for income up to €7,479 and reaches 48% for amounts exceeding €81,199 annually. Residents must report worldwide income, meaning rental earnings from your Algarve villa plus any foreign salary or investment returns all count toward your total taxable income. This worldwide taxation scope gives residents access to personal deductions, family allowances, and expense offsets that reduce the final tax bill.

Non-residents get a simpler but less flexible deal. Portuguese tax law imposes a flat 28% rate on rental income sourced from Portuguese properties. You pay this rate regardless of whether you earn €5,000 or €500,000 in annual rental income. No progressive brackets, no personal deductions, no expense offsets. The tax applies to gross rental income, making your effective tax burden higher than it appears at first glance.

The legal criteria for determining tax residency include:

- 183-day rule: Spending more than 183 days in Portugal during any 12-month period starting or ending in the tax year

- Permanent residence test: Maintaining a habitual residence in Portugal under circumstances suggesting intent to keep it

- Economic ties: Having your center of economic interests in Portugal, such as primary business activities or family residence

- Deemed residency: Being registered as a resident for any purpose may trigger tax residency classification

Filing and reporting obligations differ substantially. Residents must submit annual IRS returns by June 30 of the following year, declaring all income sources worldwide. Non-residents face simpler requirements but must still file if they have short-term letting tax implications or other Portuguese income. The tax residency rules Portugal applies determine your entire tax strategy, from entity structuring to deduction planning.

2026 rental income tax reforms and their impact

Portugal’s 2026 budget introduced dramatic changes targeting long-term rental supply. The government reduced the IRS tax rate to just 10% for qualifying long-term rental contracts. This reform aims to incentivize landlords to shift properties from short-term tourist rentals to stable long-term housing. The catch? Strict eligibility requirements limit who can benefit.

To qualify for the 10% IRS rate, landlords must meet specific criteria:

- Register the rental contract with tax authorities (Autoridade Tributária) before tenants move in

- Cap monthly rent at €2,300 or below

- Lease the property on a long-term basis, typically 12 months or longer

- Own the property as an individual, not through a corporate entity

- Comply with rent increase limitations tied to inflation indices

The €2,300 monthly rent cap presents challenges in premium Algarve markets like Lagos and Vilamoura, where luxury properties command higher rents. Properties exceeding this threshold default to standard progressive IRS rates for residents or the 28% flat rate for non-residents. This rent ceiling effectively excludes high-end investment properties from the reduced rate benefit.

Contract registration requirements add administrative burden but create transparency. You must submit lease agreements through the tax authority’s online portal, including tenant details, rent amounts, and contract duration. Failure to register disqualifies you from the 10% rate and may trigger penalties.

Critical statistic: The 2026 reforms also increased the IMT (property transfer tax) for non-resident buyers to 7.5%, up from previous rates. This raises your acquisition costs by thousands of euros on typical Algarve investment properties.

Rent increase caps further constrain landlord flexibility. Annual rent adjustments cannot exceed official inflation indices, limiting your ability to capture market appreciation. These restrictions trade short-term income growth for long-term tax savings.

Compliance steps to benefit from reforms:

- Verify your property qualifies under the €2,300 rent cap

- Register your lease contract through the AT portal within legal deadlines

- Maintain documentation proving contract terms and tenant occupancy

- File annual IRS returns claiming the 10% rate with supporting evidence

- Monitor compliance with rent increase limitations

- Consult tax advisors if ownership structure or residency status changes

These reforms fundamentally reshape rental investment strategy. Properties suited for long-term property investment now offer compelling after-tax returns if you can work within the regulatory framework. Short-term rentals face higher effective tax rates, making the financial comparison between strategies more complex.

Allowable deductions to optimize rental taxation

Resident landlords can deduct legitimate expenses against rental income before calculating tax owed. This reduces your taxable income substantially if you maintain proper records. Allowable deductions include property maintenance costs, IMI municipal property tax, insurance premiums, rental management fees, and utility costs incurred while the property sits vacant between tenants.

Typical deductible expense categories include:

- Property maintenance and repairs: Painting, plumbing fixes, appliance replacements, garden upkeep

- IMI property tax: Annual municipal property tax paid to local authorities

- Insurance: Building insurance, contents insurance, liability coverage

- Management fees: Payments to property managers or rental agencies

- Utilities during vacancy: Electricity, water, internet when property is empty

- Professional fees: Accountant costs for tax preparation, legal fees for lease drafting

- Depreciation: Annual depreciation deductions on property value over time

Non-residents face a harsh reality. The flat 28% tax applies to gross rental income with zero deductions allowed. You cannot offset insurance, maintenance, management fees, or any other expense against your rental earnings. This makes the effective tax burden significantly higher than the nominal 28% rate suggests.

Proper documentation is essential for residents claiming deductions. You need invoices (faturas) with your Portuguese tax number (NIF) clearly listed. Receipts without proper NIF registration get rejected during audits. Store digital copies of all expense documentation for at least five years, the standard audit lookback period.

Pro Tip: Set up a dedicated bank account for rental income and expenses. This creates a clean paper trail showing all transactions flow through one account, making year-end reconciliation and audit defense much simpler.

Common pitfalls that trigger deduction rejections:

- Personal expenses mixed with rental expenses (claiming your own vacation stay costs)

- Missing or incomplete invoices without proper NIF registration

- Capital improvements misclassified as repairs (renovations add to property basis, not current deductions)

- Excessive expense claims that appear unreasonable relative to rental income

- Failing to distinguish between deductible repairs and non-deductible improvements

Understanding property tax info for foreign buyers helps you plan which expenses qualify and how to structure your affairs. The difference between gross and net rental income determines whether your investment generates positive cash flow or requires ongoing capital injections. For residents, aggressive but legitimate deduction planning can cut your effective tax rate substantially compared to the statutory brackets.

Resident vs non-resident taxation on rental income

The tax treatment diverges sharply based on residency status. This comparison table clarifies the key differences:

| Facteur | Tax Resident | Non-Resident |

|---|---|---|

| Tax rate | Progressive IRS brackets (12.5% to 48%) | Flat 28% on rental income |

| Income scope | Worldwide income taxed in Portugal | Only Portuguese-sourced income |

| Deductions allowed | Yes, maintenance, IMI, insurance, management fees | No deductions permitted |

| Filing deadline | Annual return by June 30 | Simpler filing, often handled by withholding |

| Eligibility for 10% rate | Yes, if individual owner meets criteria | Yes, if individual owner meets criteria |

| Documentation requirements | Comprehensive worldwide income reporting | Portuguese rental income only |

Non-resident landlords pay the flat 28% tax on gross Portuguese rental income without any expense relief. Meanwhile, residents report worldwide earnings and pay progressive tax but gain deduction access. This creates strategic planning opportunities around residency timing and ownership structuring.

The worldwide income obligation for residents means your UK salary, French dividends, or German rental income all get declared on your Portuguese return. Portugal provides foreign tax credits to prevent double taxation under bilateral treaties, but you still face Portuguese tax on the total if it exceeds foreign taxes paid. Non-residents avoid this complexity but sacrifice deduction benefits.

Compliance and documentation requirements scale with complexity. Residents need detailed records of all income sources, foreign tax payments, deductible expenses, and family circumstances affecting personal allowances. Non-residents only track Portuguese rental income and ensure proper withholding or direct payments to tax authorities.

This residency classification influences major investment decisions. Should you establish Portuguese residency to access deductions and lower effective rates? Should you time property purchases around residency status changes? Should you structure ownership through entities to manage tax exposure? These questions require careful tax planning for long-term rental success.

Accurate residency classification prevents penalties and optimizes outcomes. Investors who misclassify themselves as non-residents when they meet residency tests face back taxes, penalties, and interest charges. Conversely, claiming resident status incorrectly triggers worldwide income reporting obligations you may not want. Get independent verification of your status before filing.

Interaction with non-habitual residency (NHR) regime

Portugal’s Non-Habitual Residency (NHR) regime historically provided generous tax breaks for new residents. Foreign professionals and retirees flocked to Portugal to access income tax exemptions and reduced rates. The 2026 budget reforms narrowed NHR benefits substantially, especially for rental income.

The 2026 NHR reforms focus eligibility on high-value professional activities, such as specialized technical work, executive roles, or scientific research. Passive rental income no longer qualifies for broad NHR exemptions. If you hold NHR status and earn rental income from Algarve properties, that income faces standard IRS taxation under resident rules. You can still access the 10% reduced rate if you meet eligibility criteria, but NHR itself no longer shields rental earnings.

Key NHR 2026 changes affecting rental investors:

- Rental income explicitly excluded from NHR tax exemptions

- Professional income must derive from high-value activities to qualify for benefits

- Existing NHR beneficiaries grandfathered until their 10-year term expires

- New applicants face stricter qualification standards

- Foreign pension income still receives favorable treatment under specific conditions

For foreign investors holding rental properties in the Algarve, NHR status provides limited rental income advantages. You still benefit from the 10% rate on qualifying long-term leases as an individual resident, just like any other resident. NHR’s value now centers on professional or pension income tax treatment, not rental earnings.

When NHR still provides tax advantages:

- You receive foreign pension income qualifying for NHR exemptions

- You earn professional income from high-value activities conducted in Portugal

- You hold foreign financial assets generating dividends or capital gains subject to NHR rules

- You structure your affairs to leverage NHR benefits on non-rental income while optimizing rental taxation separately

Monitor your NHR eligibility and benefits annually. The regime’s complexity and frequent rule changes require ongoing professional guidance. Don’t assume NHR automatically improves your rental income tax position in 2026. Run the numbers comparing NHR resident status versus non-NHR resident status to verify actual benefits.

Common misconceptions about rental income tax in Portugal

Foreign investors frequently misunderstand Portuguese rental tax rules, leading to costly errors. Let’s debunk the most common myths.

Misconception 1: Non-resident landlords can claim expense deductions to reduce their 28% tax burden. False. Non-residents pay 28% on gross rental income with zero deductions allowed. You cannot offset maintenance, insurance, management fees, or any other costs against rental earnings.

Misconception 2: All rental income qualifies for the new 10% IRS rate. Wrong. Only individual landlords with registered long-term lease contracts capped at €2,300 monthly rent qualify. Short-term rentals, corporate-owned properties, and leases exceeding the rent cap default to standard tax rates.

Misconception 3: Company-owned rental properties benefit from the 10% reduced rate. Incorrect. The 10% IRS rate exclusively applies to individual landlords. Companies owning rental properties face corporate income tax (IRC) rules. While some corporate structures may access partial tax reductions, they do not qualify for the 10% individual IRS rate.

Misconception 4: Establishing a Portuguese company shields rental income from high taxes. Partially false. Portuguese companies pay IRC corporate tax rates, currently around 21% plus municipal surcharges. While potentially lower than high-bracket IRS rates for individuals, corporate structures add compliance costs, administrative burden, and restrict personal use of properties. The 2026 reforms offer corporations a 50% IRC reduction on long-term rental income under specific conditions, but this still exceeds the 10% individual rate.

Misconception 5: Residency status doesn’t matter if you own property through a foreign entity. False. The location and structure of the owning entity affects taxation, but rental income sourced from Portuguese properties remains taxable in Portugal regardless of owner nationality or entity domicile. Residency status determines your tax rate and obligations, not the entity structure.

Pro Tip: Verify all tax information directly from official sources or qualified Portuguese tax advisors. Online forums and expat groups often repeat outdated or incorrect guidance that leads to non-compliance.

Misinterpreting residency status causes widespread filing errors. Investors who spend summers in Portugal but maintain primary homes abroad often incorrectly assume non-resident status. The 183-day test and permanent residence criteria catch many by surprise, triggering worldwide income reporting obligations they didn’t anticipate.

Before making tax planning decisions, confirm current rules with professionals specializing in Portuguese cross-border taxation. The 2026 reforms introduced substantial changes that invalidate older advice. What worked in 2024 may no longer apply in 2026.

Practical steps for foreign investors to optimize rental income tax

Maximizing after-tax rental income requires systematic planning and compliance. Follow these steps to optimize your tax position.

Step 1: Determine your residency status accurately. Track days spent in Portugal using calendar records and travel documents. If you meet the 183-day test or maintain a permanent residence, you qualify as a tax resident. This classification determines your entire tax strategy.

Step 2: Classify your rental contract for reduced IRS rate eligibility. Review your lease terms against the 10% rate criteria: registered contract, €2,300 monthly rent cap, long-term duration, individual ownership. If you qualify, register the contract immediately through the Autoridade Tributária portal.

Step 3: Evaluate ownership structure benefits. Compare individual ownership versus corporate entities:

- Individual ownership: Access to 10% IRS rate on qualifying leases, simpler administration, personal use flexibility

- Corporate ownership: Potential asset protection, estate planning benefits, but higher tax rates and no 10% IRS qualification

Step 4: Maintain detailed accounting of all rental-related transactions:

- Income: Record every rent payment with dates, amounts, and tenant details

- Expenses: Collect invoices with your NIF for maintenance, insurance, IMI, management fees

- Contracts: Store signed lease agreements, registration confirmations, amendment records

- Correspondence: Keep tenant communications, repair requests, inspection reports

Step 5: Stay informed on legal reforms and update your strategy accordingly. Portuguese tax law changes frequently. Subscribe to updates from tax advisory firms, monitor official government announcements, and review your strategy annually with professionals.

Step 6: Consult qualified tax advisors for complex situations. Seek professional guidance when:

- Your residency status is uncertain or changing

- You own properties through foreign entities

- You claim NHR benefits

- You have multiple income sources across countries

- You face audit inquiries or compliance disputes

Practical optimization tips:

- Time property acquisitions and sales around residency status to minimize IMT and capital gains taxes

- Structure lease terms to qualify for the 10% rate without sacrificing too much rental income

- Maximize legitimate deductions if you’re a resident by maintaining meticulous records

- Consider long-term rental returns versus short-term rental yields after accounting for tax differences

- Leverage property tax strategies for foreign buyers when negotiating purchase terms

Don’t let tax considerations alone drive investment decisions. Evaluate property fundamentals, market dynamics, rental demand, and personal goals alongside tax optimization. A property generating strong pre-tax returns with higher taxes often outperforms a weak property with minimal tax exposure.

Optimize your Algarve property investment with Riva Prime

Navigating Portugal’s complex rental income tax rules demands local expertise and ongoing compliance support. Riva Prime specializes in maximizing after-tax returns for foreign investors targeting the Algarve market. Our team understands the 2026 tax reforms, residency implications, and strategic structuring options that optimize your rental income. We provide tailored consulting covering property investment tips for EU buyers, tax planning, and compliance management.

Beyond tax optimization, our comprehensive property management in Lagos services handle tenant placement, contract registration, rent collection, maintenance coordination, and annual tax reporting. We ensure your investment meets all 10% IRS rate requirements while maximizing occupancy and rental income. Our long-term property investment strategies integrate tax efficiency with market positioning to deliver superior risk-adjusted returns. Contact Riva Prime today to build a rental income tax strategy that protects your capital and accelerates wealth accumulation in Portugal’s premier coastal region.

FAQ

How is rental income tax calculated for non-resident investors in Portugal?

Non-residents pay a flat 28% tax on gross rental income from Portuguese properties. No deductions are permitted, meaning the tax applies to total rent collected without offsets for expenses like maintenance, insurance, or management fees. This makes the effective tax burden substantially higher than the nominal 28% rate.

What are the eligibility criteria for the 10% IRS tax rate on rental income?

The 10% IRS rate requires a registered long-term lease with monthly rent capped at €2,300. You must own the property as an individual, not through a corporate entity. The contract must be registered with tax authorities before tenants occupy the property, and rent increases are limited to official inflation indices.

Can company-owned properties benefit from the 10% reduced IRS rental tax rate?

No. Company-owned rental properties are taxed under corporate income tax (IRC) rules, not the individual IRS system. While companies may access a 50% IRC reduction on qualifying long-term rental income, they cannot claim the 10% IRS rate reserved exclusively for individual landlords. Corporate structures face different compliance requirements and typically higher effective tax rates on rental income.

What records should foreign investors maintain for rental income tax purposes?

Keep invoices for all expenses including maintenance, management fees, property insurance, and IMI municipal tax payments. Ensure every invoice includes your Portuguese tax number (NIF). Store signed lease agreements, contract registration confirmations, and payment records for rent received. Maintain these records for at least five years to support tax filings and defend against potential audits.